There is a Bubble

The AI hardware cycle is repricing risk the market hasn’t priced yet. FCC has been building its portfolio around exactly this scenario for eighteen months.

Please before diving in, read this disclaimer.

There Is A Bubble, we know because we studied the last one.

Future Cognitive Capital tracks a specific class of company: those that treat proprietary behavioral data as their primary raw material, compounding durable intelligence advantages over time. Every piece published here is one node in that thesis. If you’re new, start here:

This article is the continuation of this one:

We want to be careful with the word bubble. It gets used carelessly, usually by people who want to sound contrarian without doing the work. It gets attached to things that are merely expensive, or merely speculative, or merely exciting. We’ve known tons of ‘Bubble’ since month, those are not bubbles. A bubble is something more specific.

A bubble is a structural mismatch between what is being priced and what can actually be delivered, sustained by a narrative that survives as long as capital keeps flowing.

Also recently, we argued that The Agent Economy Is Built on Sand.

And Hidden Market Gems, 6 months ago, wrote this about OpenAI, which is still valid.

And by that definition, we think there is a bubble in AI.

Not in the technology because the technology in itself is real. Not in the companies that have built genuine, defensible positions around data and proprietary intelligence. We took the time to explain it to you here:

Some of those are, in our view, among the best long-term holdings available in public markets.

The Bubble

The bubble is in something more precise: the hardware layer, the pure-play model companies, and the infrastructure plays that depend on assumptions about returns that the numbers, right now, do not support.

We don’t want to make a crash prediction, because:

“Markets can remain irrational longer than you can remain solvent.”

―John Maynard Keynes.

We want to say that the structure of the current cycle contains the same fragilities that have ended every technology infrastructure boom in history, and that serious investors should understand what those fragilities are, where they sit, and how to position around them rather than through them.

That is what FCC was built to do. And it is what this article is going to show you, in detail, with data because we want to stay precautious.

I. What Future Cognitive Capital Is, and Why This Conversation Starts Here

Before we get to the bubble, a word about who is speaking and why it matters.

Future Cognitive Capital is an investment research publication built around a single thesis: in the current technological cycle, the companies that will compound the most durable value are the companies that treat proprietary data as their primary raw material, the ones that build systems where every user interaction makes the product smarter, and where that accumulated intelligence becomes structurally impossible for competitors to replicate.

That is our postulate. The postulate that drove every investment decision since 2024.

We call this a cognitive moat. The term matters because it is different from a traditional competitive moat. A traditional moat is a barrier: patents, brand, switching costs, network effects.

A cognitive moat is something more dynamic.

A cognitive moat is a system that actively learns, that gets harder to displace with each passing quarter, not because of legal protection but because of accumulated intelligence that a newcomer simply cannot acquire by throwing money at the problem.

To evaluate these companies rigorously, we built an eight-dimension scoring framework. We score every company we cover across data quality, intelligence layers, behavioral architecture, feedback loops, modular architecture, full-stack control, out-of-distribution generalization, and last but not least, financial quality (even if, let’s be true, financial quality is more the result of the eight dimensions and help us quantity market asymetry).

Each cognitive dimension is scored out of five, financial quality out of ten, for a total of fifty points. It is not a perfect instrument and we know it, nothing in investment analysis is, but it forces a discipline that most equity research does not apply: it asks whether a company’s competitive advantage compounds over time, or merely persists.

Here are our scores, we have 10 companies in the portfolio, but soon, 11. The piece is indeed in preparation.

We mention this because the argument we are about to make about the AI bubble is not based on macroeconomic intuition or trend-watching.

It flows directly from applying this framework to what is currently happening in the AI infrastructure market, and asking a simple question: where, in this entire ecosystem, does cognitive capital actually compound?

The answer is more concentrated, and more counterintuitive, than most investors currently believe…

But we see the counterargument coming: ‘but you’ll miss incredible performance in hardware, AI is the future’. To which we answer, without giving extra time to this fallacious argument: Cisco, was an incredible performance too. It’s not that we are closed to conversation, but again, you have to read HMG’s investment thesis to understand our view:

II. The Four Structural Fragilities

We identified indeed four structural weaknesses to the AI bull thesis.

We will sound extraordinary dumb as almost everything we will address and confront is taking +20% every session. But we will remain real to our framework and our convictions.

1. The Hardware Depreciation Problem Nobody Wants to Discuss

Let us start with the most concrete issue.

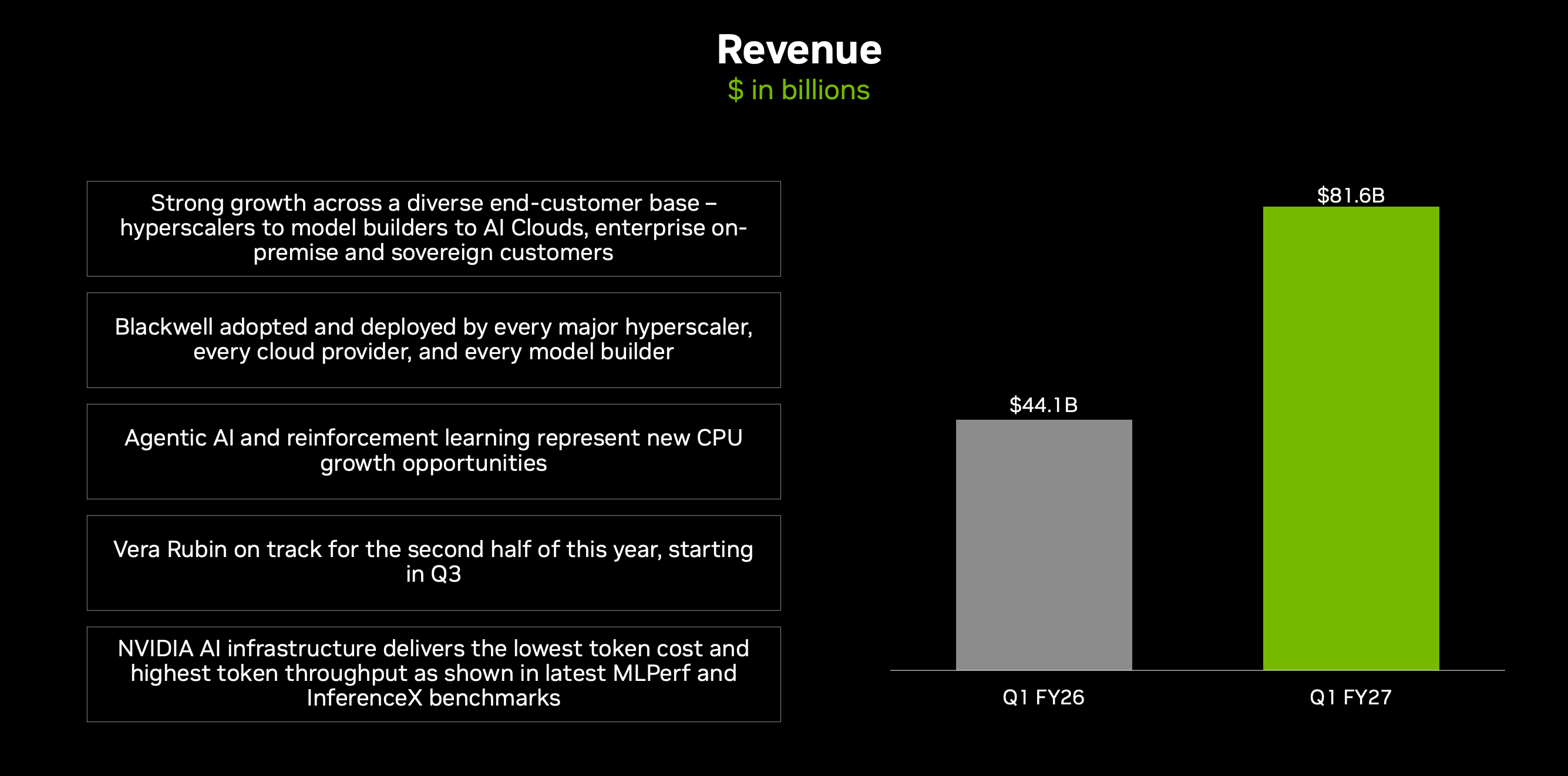

NVIDIA, as of late May 2026, carries a market capitalisation of approximately $5.2 trillion. That number has made it, briefly, the most valuable company in the world. The justification offered is: AI demand is infinite (in a finite world), NVIDIA makes the best chips for AI (it not that they are the only ones that made chips that are that good…), therefore NVIDIA’s revenue will grow indefinitely, therefore the valuation is deserved.

Look at last quarter:

The problem with this reasoning is that it ignores what NVIDIA itself is doing to the market. In fact, NVIDIA has shifted to an annual product release cadence. Hopper (2022), Blackwell (2024), Rubin (2026), with Rubin Ultra already on the roadmap for 2027. Each new generation does not merely improve on the last but renders it obsolete as a frontier compute asset.

Do you follow us on this? Then:

When Blackwell arrived, H100 cloud rental rates fell from a peak of $8 to $10 per GPU-hour to approximately $3.11 per GPU-hour in early 2026, with spot instances touching $1.25. That is a price collapse of more than 60% in under two years.

So stop the teasing, here is why that matters beyond the obvious: the hyperscalers, those are the very large cloud and AI infrastructure companies such as Amazon, Microsoft, Google, Meta, and Oracle, collectively committed to spending somewhere between $600 and $690 billion in capital expenditure on AI infrastructure in 2026 alone. A meaningful fraction of that spending is on GPU hardware, hardware that will begin losing economic value before it is fully depreciated on anyone’s balance sheet.

$176 billion, The GDP of Kuwait, will vanish.

Michael Burry, here on Substack and the investor known for correctly anticipating the 2008 mortgage crisis before it happened, has estimated approximately $176 billion in understated depreciation across the AI infrastructure industry.

That figure, if it proves accurate, represents losses that have not yet appeared in any earnings release. What is remarkable about the current situation is that Amazon and Meta, two of the largest GPU buyers in the world, could not agree in the same quarter on how long a GPU actually lasts for accounting purposes.

Amazon shortened its estimated server useful lives in 2025. Meta extended them. Same technology, same quarter, opposite accounting decisions. That is not a sign of an industry with a settled understanding of its own asset economics.

Born to Destroy

NVIDIA’s annual release cadence is, structurally, a mechanism for destroying the economic value of the hardware it has already sold. This is good for NVIDIA’s revenue. It is not necessarily good for the entities that bought the previous generation and are now holding depreciating assets on their balance sheets while managing the question of when to upgrade to hardware that will itself be obsolete within eighteen months.

By the way, a good contradiction and additions of some of these point we initially made:

2. The OpenAI Problem, Which Is Not Actually About OpenAI

OpenAI is currently valued at approximately $852 billion, more than Ireland GDP and a bit less than Taiwan’s. It is generating roughly $2 billion per month in revenue.

It is projected to lose $14 billion in 2026, roughly three times its estimated losses for 2025. It does not expect to reach profitability until 2029 at the earliest. Also, it doesn’t have a proper business model (clearly identify). You can be sure that even if you call it the future, no VC crazy enough would invest in that looking at the pitch deck. We might be too conservative, as some eventually did…Anyway. Internal projections, reported by The Information, suggest cumulative losses of $44 billion between 2023 and the end of 2028, with some revised estimates suggesting losses could reach $115 billion before the business becomes sustainably profitable in the early 2030s.

Let us make sure those numbers are clear. A company generating $24 billion in annualised revenue is valued at $852 billion, and will lose $14 billion this year. That is a loss-to-revenue ratio of roughly 58%. The company’s own burn rate is projected to stay at 57% of revenue through 2027.

The standard response to this is that it does not matter because growth is so explosive, and revenue is growing exponentially. This is, in some narrow sense, true. OpenAI went from $28 million in annual revenue in 2022 to over $20 billion in annualised revenue by mid-2026. That growth rate is historically extraordinary.

But growth without a path to unit economics is not a business. And the structural problems with OpenAI’s model are not solvable with more revenue, because the costs grow with the revenue. Every time a user runs a query, OpenAI pays for compute. Every time a user asks a harder question, OpenAI pays more for compute.

So in plain english: the product that generates revenue is also the product that generates cost, in a ratio that does not currently converge to profit without a fundamental change in the cost structure of inference, which is the process of running a trained AI model to generate an answer.

OpenAI also faces a competitive environment that is structurally different from twelve months ago. Claude, Gemini, and Llama, Chinese models, the open-source model released by Meta that anyone can run for free, are all eroding the assumption of ChatGPT’s indispensability.

In Q1 2026, OpenAI posted a negative 122% non-GAAP operating margin. ChatGPT’s user growth has stalled. Anthropic, which builds Claude and the model we are using to help produce our research for instance, passed OpenAI in annualised revenue run-rate in April 2026, reaching $45 billion ARR while spending significantly less on model training. So do see it coming?

Crystal thinks the valuation of $852 billion for OpenAI encodes a belief that one of these companies will become the dominant AI platform of the next decade, in the way that Google became the dominant search platform or AWS became the dominant cloud infrastructure. We all agree hat outcome is possible and it may even be probable for one of the frontier model companies.

But we also all agree that it is not probable for OpenAI specifically, and it is not compatible with a $852 billion valuation for a company that is currently losing money at this scale and facing genuine competitive pressure from a better-capitalised, faster-growing rival.

OpenAI is preparing for an IPO, currently targeted for late 2026 or 2027. An IPO is a liquidity event for early investors. It is not evidence of business model maturity… We believe this will be a catastrophe, the structure of the valuation, the losses, the competitive dynamics, and the IPO timeline all point in the same direction: the people who funded OpenAI in its early rounds need an exit.

The public market is the mechanism for that exit. This is, in fact, exactly what happened with many of the most prominent dot-com era companies: real technology, genuine early traction, and a listing that transferred risk to public investors at the moment when private investors could no longer justify holding. For instance, Hidden Market Gems is still in disbelief regarding Figma, but hopefully he is still a serious investor with a track record, at least not for this time…

3. The Supply Chain Is Not Secure

This one is discussed less frequently, because it is uncomfortable and not really understand by everyone. The manufacture of advanced AI accelerators depends on a supply chain that is geographically concentrated in ways that create systemic risk.

TSMC, the famous Taiwanese company that fabricates the most advanced chips in the world, including NVIDIA’s GPUs, manufactures approximately 90% of the world’s most advanced semiconductors. It is located in Taiwan.

The manufacture of High Bandwidth Memory, the specialised RAM that every modern AI accelerator requires, is controlled by three companies: SK Hynix in South Korea, Samsung in South Korea, and Micron in the United States. The advanced packaging processes that assemble these components into working systems are largely concentrated in Asia.

| Micron Technology Inc.")

The bottleneck for AI infrastructure in 2026 is no longer GPU chip fabrication. It has moved upstream to HBM memory, which has seen demand grow five times between 2023 and 2026 while supply has been structurally constrained. HBM requires two to three times more silicon area per gigabyte than standard DRAM, uses specialised stacking processes with lower manufacturing yields, and cannot be meaningfully ramped in under two to three years.

Just look at the crazy valuation all the supply chain of AI and memory is going through, even for small and micro cap without revenue… it is completely insanity.

Every quarter without a supply disruption is, in this context, the absence of a bad event, but not evidence that the risk does not exist…We are not predicting a geopolitical crisis but we are noting that the entire economics of the AI hardware cycle depends on a supply chain that investors in NVIDIA or AI infrastructure ETFs have essentially no pricing of in their current positions.

And it looks like china will not let Taiwan go so easily.

4. The Returns Are Not There Yet

This is the most important structural issue, and the one most consistently ignored because everyday the market give us reason to look elsewhere.

The global AI infrastructure build-out of 2024 to 2026 is justified, in the public narrative, by the assumption that AI-driven productivity gains will generate enormous economic returns across every industry. We all agree on that, that assumption may be correct. But the operative word is “may,” and the returns have not, at this point, materialised at the scale required to justify $690 billion in annual capital expenditure.

Yes, even ourselves are saying that.

Goldman Sachs published an analysis in 2024 asking whether $1 trillion in AI infrastructure spending would ever pay off. The answer was not a definitive yes. Even Goldman Sachs starts to show doubts.

More recent research has identified a growing gap between AI infrastructure investment and measurable productivity improvements at the macroeconomic level. AI is, without question, making individual workers more productive at specific tasks. It is not yet demonstrably transforming the GDP-level productivity statistics in any major economy.

The venture capital market has absorbed more capital than at any point in its history. In 2025, AI companies attracted $258.7 billion in global venture investment, representing 61% of all global VC activity, up from 30% in 2022. The top five deals alone accounted for $63 billion, with mega-deals comprising 73% of total AI VC value. This is the capital concentration pattern of a late-stage bubble, not of a market still in early price discovery.

III. The Form Is Familiar, Even If the Content Is Not

We are not saying this is 2000, or are we?. The people who say it is exactly 2000 are being lazy in the same way that the people who say it cannot possibly be 2000 are being lazy, maybe we are lazy?

History does not repeat precisely, it’s not coincidence, the universe is rarely so lazy. But it rhymes, and the rhyme here is at least, audible.

Let’s go back in time. In 1999, the build-out of internet infrastructure consumed an enormous amount of capital. Cisco, Nortel, and Lucent were valued as if the demand for fibre optic cable, routers, and switching equipment was infinite and permanent (it cannot, it’s hardware). The demand for connectivity was real.

What was not real was the assumption that the equipment vendors who built the infrastructure would capture permanent, compounding value from doing so. When the demand pause arrived, as it always does when any technology reaches the temporary plateau before the next wave of adoption, the equipment vendors collapsed. Cisco fell 86% from peak to trough. Nortel went bankrupt, the companies that survived and compounded value were the ones that owned the application layer built on top of the infrastructure: Google, Amazon, Salesforce…. Hmm sounds familiar with a certain thesis, does it?

So our point is: the structure here is recognisable. The hardware vendors of the current cycle, NVIDIA, ASML, the GPU cloud providers, are being valued as if the demand for AI accelerators is infinite and permanent. The application and data layer companies, the ones actually building compounding cognitive moats, are in some cases valued more reasonably.

The dynamic is the same but indeed the specific numbers and companies are different.

What is genuinely different in 2026 versus 2000 is the balance sheet quality of the largest players. Amazon, Alphabet, and Microsoft are not Nortel. They have real revenue, real cash flow, and real businesses that exist independently of the AI build-out. If AI disappoints in the next two years, they will not go bankrupt. They will take write-downs, and they will pivot, and they will survive. That is a meaningful structural difference.

But the pure-play hardware companies, the model companies without viable unit economics, and the infrastructure plays whose entire valuation rests on AI demand remaining at 2024-2026 levels indefinitely: those carry the fragility profile that every previous infrastructure bubble has eventually resolved…

If this framework changes how you read the tech landscape, FCC was built for you. Subscribers get full scoring, portfolio positions, and weekly signal analysis.

IV. What FCC Built Instead

This is where the argument becomes concrete.

Eighteen months ago, working from the framework described above, Future Cognitive Capital began constructing a portfolio built around a specific answer to a specific question: if you accept that the hardware layer of AI is entering a commoditisation cycle, and that the pure-play model companies have structural unit economics problems, where does cognitive value actually compound?

Data over Chips

After careful consideration and research, the answer was not in the chips but in the data.

Some disclaimer: not really the common data as a buzzword meaning.

But as a raw material, which means: data as a specific, technical, structural asset: proprietary data generated by real people doing real things on real platforms, at a scale and specificity that makes replication structurally impossible regardless of how many GPUs a competitor purchases.

How we know this is the way? Mistral’s CEO, the French model competing ChatGPT clearly stated that their model performance was reaching ChatGPT’s for a moment with no compute and no fund like OpenAI, because they invested a lot in data cleaning, structuring, labelling…

So the company that has ten years of how 500 million users book travel, or how every police officer in the United States interacts with evidence at a crime scene, or how every small merchant manages their inventory and customer relationship, does not lose that advantage when a new GPU architecture ships.

The advantage is not in the chip.

The advantage is in the accumulated intelligence that the chip cannot generate from scratch!

Ten companies currently sit in the FCC portfolio, soon, 11. They do not all hold the position for the same reason. But each of them passes the central test: their competitive advantage is not a function of which generation of hardware they are currently running.

Here is what each of them is, why they are in the portfolio, and why we believe they are structurally positioned to survive and compound through the scenario described above.

This is the end of the free tier of this article, if you interested of knowing these company, you can go deeper. At least we hope you find these arguments interesting and that you’ll keep them in mind when allocating or opening you next position. If you subscribe now, you’ll soon get the last FCC company file that are finishing when we write these lines.

That is a good occasion we present the whole 10 company ans why we have them.

If you want to know these tech company that are AI-Bubble proof, it’s now.